Wealth Planning Insights

New Wealth – Strategies for Financial Windfalls

Adam Lawrence, CPA, CFP®, May 2026

National Championships, Inheritances and Retirement have One Thing in Common

In January 2026, Fernando Mendoza, the Indiana Hoosiers' Heisman–winning quarterback, led an historic run to a National Championship. While the victory secured his place in the record books, it also fundamentally shifted his balance sheet. Overnight, his NIL (Name, Image, and Likeness) valuation spiked to an estimated $2.6 million. This can already be seen in the new partnerships he’s secured with Taco Bell, LinkedIn, and Adidas, among others.

To the casual observer, this is a sports story. To a Wealth Manager, this is a Liquidity Event that results in Sudden Wealth.

Whether it is a $2.6 million endorsement deal, a $3 million inheritance, the sale of a business or retirement, the challenge remains the same: A substantial increase in one’s investable wealth is not spendable income like a salary – it is finite investable income producing capital that will benefit from a comprehensive Wealth Planning strategy.

The Anchor of Every Plan: A Planned Withdrawal Rate

The most common mistake after receiving a windfall is viewing the lump sum as a "spending fund" rather than an "income engine." To determine if a windfall can support a lifestyle, wealth recipients and their advisor can use either the Traditional Withdrawal Rate (TWR) or the Perpetual Withdrawal Rate (PWR).

Traditional Withdrawal Rate (TWR)

The Traditional Withdrawal Rate sets the highest distribution of dollars that one can withdraw in the first year of retirement (or other source of new wealth) which can be adjusted for future inflation through a preset time period (30 years, 40 years, etc.) with high confidence (greater than 90% achievable based on history).

This is often referred to as the "4% Rule" as the initial dollar amount was thought to be 4% of the total wealth supplying the income withdrawals. However, Tanglewood’s research shows that the initial percentages vary with both the time period for which the income is intended and the strategic asset allocation (Investment Policy) that one chooses to govern the investments.

Many of those experiencing sudden wealth gravitate to the TWR for its predictability of inflation–adjusted income.

Perpetual Withdrawal Rate (PWR)

This method of withdrawing income from a portfolio is more ideal for multi–generational wealth. The goal is not to maximize a stable inflation adjusted income for a set time period but to ensure that the wealth itself is maintained indefinitely with appropriate withdrawals.

This method sets an annual percentage that can be distributed from the portfolio. The percentage is determined by the strategic asset allocation chosen. Because the portfolio value changes annually with market conditions, the percentage withdrawal in any particular year is set by the past year’s investment performance of that asset allocation. The annual withdrawals from this method are more variable but also more sustainable over long, indefinite time periods.

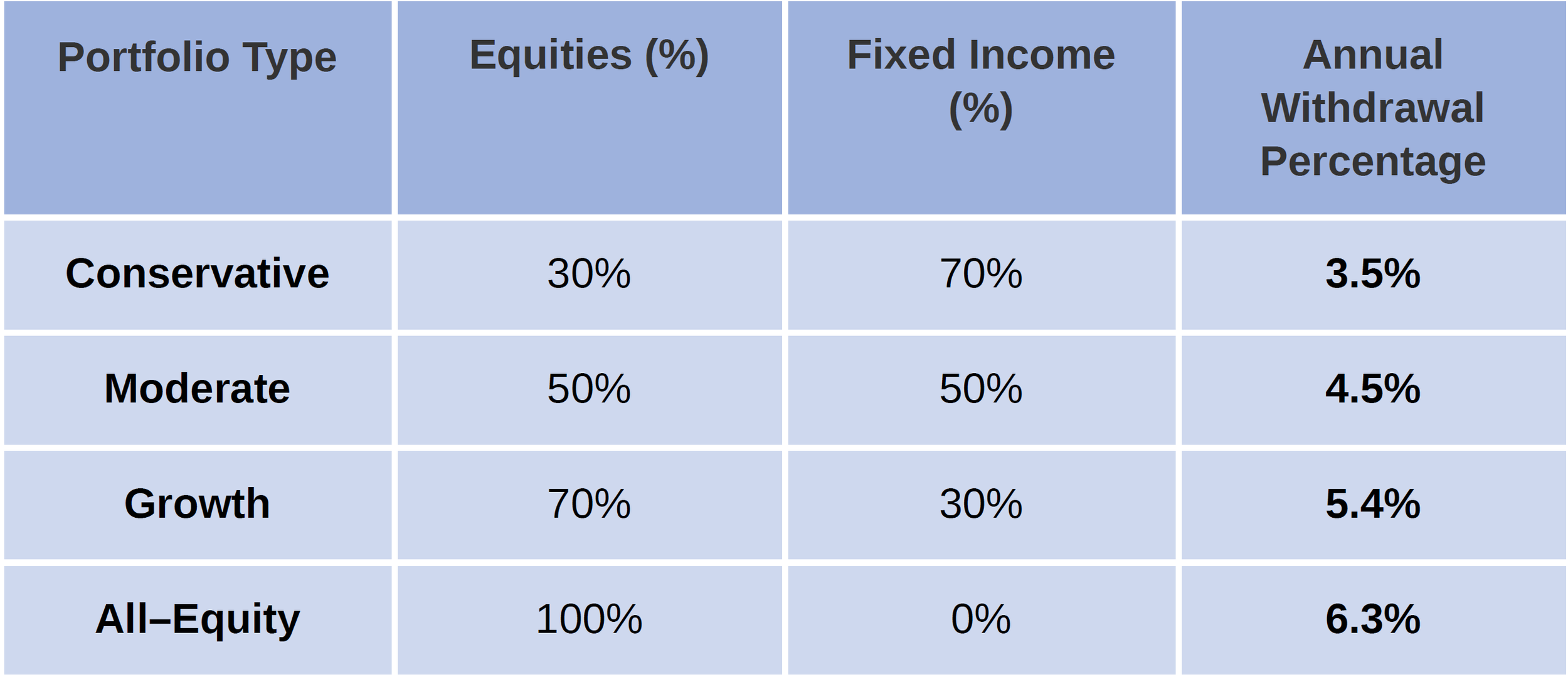

In Tanglewood’s most recent book, Perpetual Wealth: Strategies for Financial Freedom, the annual percentage withdrawal rates for four of our Investment Policies based on the beginning portfolio value are:

Why Windfalls Threaten Portfolio Integrity

A windfall often provides a false sense of security. If no plans are made for how much can be safely withdrawn from the total portfolio – based on either TWR or PWR – the overwhelming tendency is to spend too much money and deplete the portfolio (and its earning capacity) over time.